The slip you choose tells the CRA who someone is

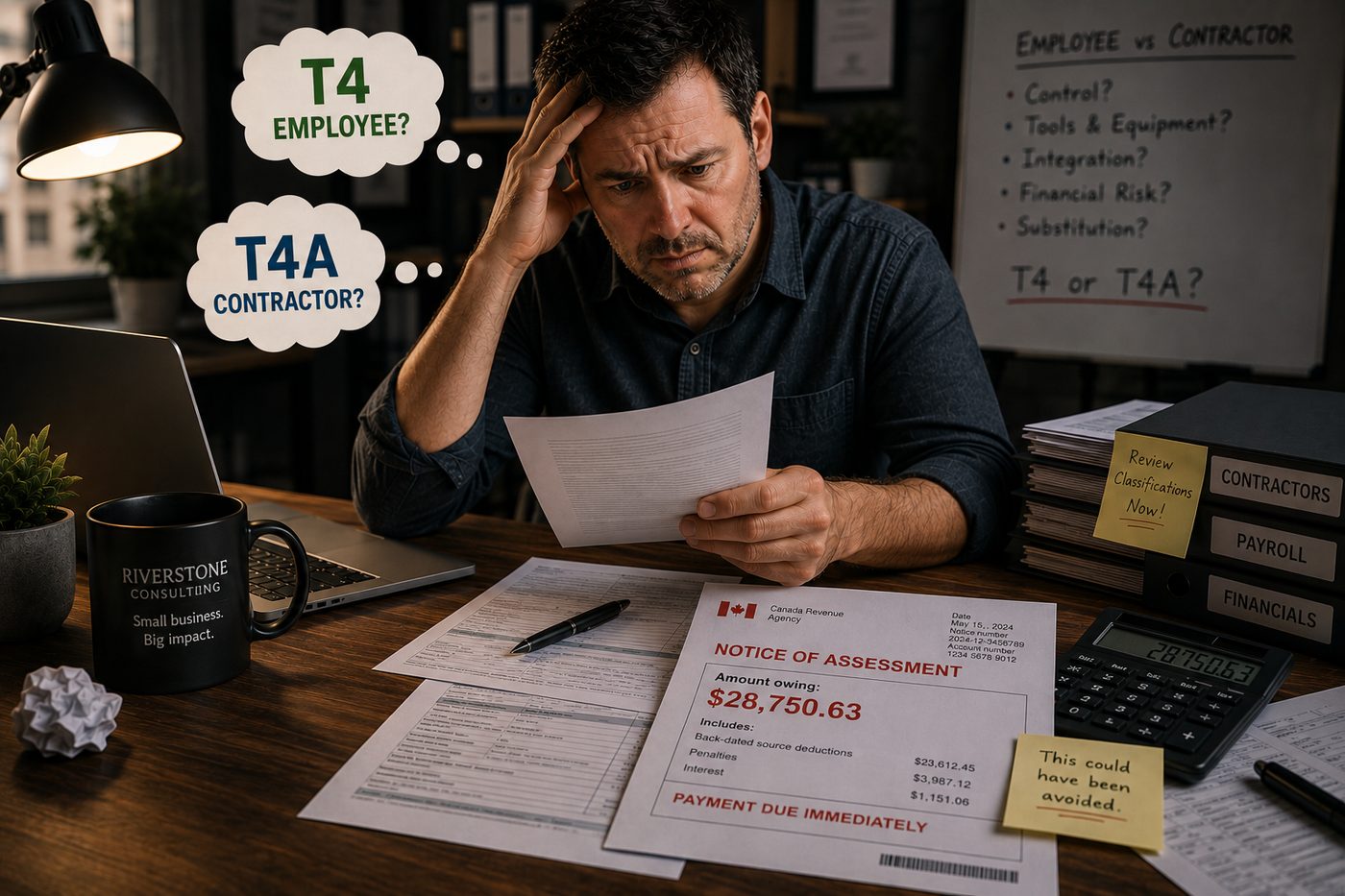

Every January, BC business owners ask us the same question: do I issue this person a T4 or a T4A? It feels like an administrative box-tick, but the answer is anything. The slip you issue is a public statement to the CRA about whether the person is an employee or an independent contractor — and if you get it wrong, the cost can be tens of thousands in back-dated source deductions, penalties, and interest.

What is the difference between a T4 and a T4A in Canada?

A T4 (Statement of Remuneration Paid) is for employees — anyone you ran payroll for during the calendar year. It reports gross pay, CPP, EI, income tax, and benefits. A T4A (Statement of Pension, Retirement, Annuity, and Other Income) is the catch-all slip for non-employment payments. For small business, the most common use is Box 048 — fees paid to unincorporated contractors over $500 in the year. The slip you issue is a public statement to the CRA about whether the person is an employee or a contractor.

When do I issue a T4?

You issue a T4 if any of these apply:

• You ran payroll for the person and withheld CPP, EI, and income tax.

• You paid an employee more than $500 in the year, even if no deductions were withheld (rare but possible — e.g., very low wages).

• You provided taxable benefits (group insurance, parking allowance, gift card over $500) — even if no cash changed hands.

Filing rules: T4 slips and the T4 Summary must be filed with the CRA and given to the employee by the last day of February (28 February in a regular year, 29 February in a leap year). If you are issuing more than five slips, you must file electronically. Late filing penalties start at $100 per slip.

When do I issue a T4A?

You issue a T4A in Box 048 (fees for services) if you paid an unincorporated individual or sole proprietor more than $500 in the year for services rendered. Examples: a freelance graphic designer, a sole-proprietor handyman, a consultant who has not incorporated.

You do NOT issue a T4A for:

• Payments to incorporated companies (they invoice you and report on their T2)

• Reimbursements for actual expenses (those are not income)

• Payments to construction subcontractors (those go on T5018, not T4A)

Other payments that get a T4A: pension and annuity payments, scholarships and bursaries, self-employed commissions, certain research grants. The CRA's enforcement of T4A Box 048 has been historically uneven but is tightening every year — issuing them properly is no longer optional.

Contractor or employee? The CRA four-factor test

This is the question that decides everything. The CRA does not care what your contract says — it cares about the substance of the relationship. Their test looks at four factors:

• Control. Who decides what work is done, when, and how? Employees take direction; contractors deliver outcomes.

• Tools and equipment. Employees usually use yours; contractors usually bring their own.

• Chance of profit and risk of loss. Contractors can make more by working efficiently or lose money on a fixed-price job. Employees cannot — they get paid for time.

• Integration. Is the worker a built-in part of your operation, or an outside provider with their own clients?

If the relationship looks and feels like employment — fixed hours, your tools, no other clients, paid by the hour for time rather than deliverables — issuing a T4A does not protect you. The CRA can reclassify the worker as an employee, assess back CPP and EI (employer AND employee portions — both become payable by you), add 10–20% penalties, and charge daily-compounded interest. We have seen BC businesses hit with $40,000 reassessments from a single misclassified worker over three years.

A simple decision flow

Ask yourself, in order:

1. Did I run payroll and withhold deductions? → T4

2. Did I pay an unincorporated person more than $500 for services and not run payroll? → T4A Box 048 (and double-check the classification)

3. Did I pay an incorporated company for services? → No slip — they invoice you

4. Did I pay a construction subcontractor? → T5018, not T4A

5. Did I provide taxable benefits to an employee but no cash? → Still T4 if the benefit is taxable

Common BC small business mistakes

• Calling everyone a contractor. Especially common in trades and hospitality. If your dishwasher works fixed shifts on your premises with your equipment, they are an employee — full stop.

• Paying a spouse without payroll. Family members can absolutely be paid, but the work must be real, the rate reasonable, and proper payroll filed.

• Forgetting T4As entirely. Many bookkeepers historically skipped them; the CRA is increasingly asking for them.

• Missing the February 28 deadline. Late filing penalties start at $100 per slip and escalate quickly. 50 slips late = $5,000 minimum.

• Confusing T5018. Construction businesses report subcontractor payments on T5018, not T4A. Different slip, different deadline, different rules.

What the boxes actually mean

Most common T4 boxes:

• Box 14: Employment income (gross pay)

• Box 16/17: CPP contributions (employee)

• Box 18: EI premiums (employee)

• Box 22: Income tax deducted

• Box 24: EI insurable earnings

• Box 26: CPP pensionable earnings

• Box 40: Other taxable benefits (group insurance, parking, etc.)

Most common T4A boxes:

• Box 020: Self-employed commissions

• Box 048: Fees for services (the big one for small business)

• Box 105: Scholarships, bursaries, fellowships

Frequently asked questions about T4 and T4A

What is a T4A used for in Canada?

T4A is used to report non-employment income — most commonly fees paid to unincorporated contractors (Box 048), pension and annuity payments, scholarships, self-employed commissions, and certain research grants. For small business, the dominant use is Box 048.

Do I issue a T4A to an incorporated contractor?

No. Incorporated contractors invoice you through their company and report the income on a T2 corporate return. You don't issue any slip — the invoice is the documentation.

What is the deadline for T4 and T4A in Canada?

Both T4 and T4A slips must be filed with the CRA and given to the recipient by the last day of February (28 February in a regular year, 29 February in a leap year). The T4 Summary or T4A Summary is filed at the same time. Late penalties start at $100 per slip.

How does the CRA decide if someone is an employee or contractor?

The CRA applies a four-factor test: control over work, ownership of tools, chance of profit/risk of loss, and integration into your business. The contract you sign is largely irrelevant — substance over form. If the relationship looks like employment in practice, the CRA will reclassify the worker regardless of what you called them.

What happens if I issue a T4A to someone who should have been on a T4?

The CRA can reclassify the worker as an employee, assess back CPP and EI (employer AND employee portions, both payable by you), add penalties of 10–20% of the source deductions that should have been withheld, and charge daily-compounded interest. Reassessments routinely run $20,000–$50,000 for a single misclassified worker over three years.

Do I issue a T4A or T5018 to a construction subcontractor?

T5018 (Statement of Contract Payments). Any business in the construction industry that pays subcontractors for construction services must file T5018 instead of T4A. Annual filing deadline is six months after your fiscal year-end, not February 28.

Do I have to issue a T4A under $500?

Technically, T4A Box 048 is only required if total payments to one unincorporated person exceeded $500 in the year. Below that threshold, you do not have to file. But many bookkeepers issue them anyway for clean records.

Can I pay my spouse and not issue a T4?

Only if (a) the work is real, (b) the rate is reasonable for the role, and (c) you run proper payroll with CPP, EI, and tax withholding. A T4 is required like any other employee. The CRA looks closely at family payroll — keep it clean.

When to talk to us before year-end

If two or more of these describe your situation, sort it before February 28 — not after a CRA letter:

• You hired anyone in the last 12 months and you're not 100% sure they're properly classified.

• You paid sole proprietors or freelancers over $500 last year and never issued T4As.

• You're in construction and have never filed a T5018.

• You pay family members and have not been running payroll for them.

• You missed last February's slip deadline and you want this year to be different.

• You hate January because it always feels like a fire drill.

Misclassification is the single most expensive payroll mistake a small business can make. Before we onboard a new worker for any client, we run a five-minute classification check using the CRA's own factors and document the conclusion. It takes almost no time and gives you a clean defence if a question ever arises.

Check our Full-service payroll, end to end at fluentbook.ca and we will sort the slips, the classifications, and the boxes before the deadline. No judgement. No surprises.